The US has destroyed an alleged cartel submarine amid tensions with Venezuela, President Donald Trump said Read Full Article at RT.com

The president earlier accused nearby Venezuela of “narcoterrorism”

The US military has destroyed a submarine in the Caribbean that was smuggling drugs, President Donald Trump said on Friday.

The statement came after the US struck at least five surface vessels since September, allegedly operated by cartels based in Venezuela, whose government Trump has accused of aiding “narcoterrorists.”

“We attacked a submarine, and that was a drug-carrying submarine built specifically for the transportation of massive amounts of drugs,” Trump told reporters at the White House. “Just so you understand, this was not an innocent group of people,” he added.

American media reported earlier that, for the first time, the US Navy picked up multiple survivors and detained them on a warship.

Trump confirmed earlier that he had authorized covert CIA operations on Venezuelan soil but declined to say whether their goal was to topple left-wing President Nicolas Maduro. The US imposed sweeping sanctions on the South American country during Trump’s first term in office and has recently raised the bounty for Maduro’s arrest to $50 million.

Maduro has rejected what he called “CIA-led coups” in the region and called for peace. “Until when will CIA coups d’état continue? Latin America doesn’t want them, doesn’t need them, and repudiates them,” he said on Wednesday, according to El Pais.

The Venezuelan government has denied ties to cartels and vowed to repel any potential invasion.

Iran’s embassy in Denmark says the continuation of sanctions on Tehran’s peaceful nuclear program will be illegal with the expiration of the UN Security Council Resolution 2231.

Britain’s Court of Appeal rules that a full judicial review of the government’s controversial ban on Palestine Action, a direct action group, can proceed next month.

The British scholar and Press TV producer David Miller has scored a “great victory” in a legal battle with the pro-Israel NGO “Campaign Against Antisemitism” that began over his pro-Palestine activism on social media.

Hungarian FM Peter Szijjarto says preparation for a summit in Budapest between US President Donald Trump and Russia’s Vladimir Putin is in "full swing".

The Swiss food giant Nestlé, which is linked to Israel, plans to cut 16,000 jobs globally, as a boycott campaign targeting the Israeli regime has expanded following its genocidal war against Palestinians in Gaza.

A visa denial by the United Kingdom has prevented Yasin Shoari, an 11-year-old Iranian table tennis prodigy, from participating in the ITTF Hopes Programme scheduled in Sheffield, England.

South Koreans are pushing back against US President Donald Trump's renewed claim this week that Seoul agreed to pay Washington 350 billion dollars for investment up front.

Yemen says its military chief of staff, Major General Mohammed al-Ghomari, has been killed following an Israeli airstrike on the capital Sana’a. Al-Ghomari played a decisive role in defending Yemen’s sovereignty and confronting US-Israeli aggression in regional waters.

Vladimir Zelensky has said he was “not happy” with Moscow’s idea of building a rail link between Alaska and Russia through the Bering Strait Read Full Article at RT.com

The Moscow-proposed project envisages a direct 70-mile route under the Bering Strait to link the two countries

Ukraine’s Vladimir Zelensky has voiced his opposition to a Moscow-proposed project to build a rail tunnel under the Bering Strait between Russia and the US.

The idea, floated by Russian presidential aide Kirill Dmitriev this week as a ‘Putin-Trump unity tunnel,’ envisages a 70-mile rail and cargo link which could unlock joint natural resource exploration.

Dmitriev, who also serves as head of Russia’s sovereign wealth fund (RDIF), invited billionaire Elon Musk to offer his Boring Company, which builds underground “Loop” transport systems.

While meeting Zelensky at the White House on Friday, US President Donald Trump told reporters that he found the idea of such a tunnel “interesting.” He then asked Zelensky for his reaction, who responded he was “not happy with it.”

The Russia-US tunnel project could cost over $65 billion, according to Dmitriev, who said that Musk’s Boring Company technology could cut it by 90% to under $8 billion and finish it within eight years. Dmitriev added that the RDIF, which helped build the first Russia-China rail bridge, was ready to take part.

BREAKING: President Trump says he finds the idea of a Putin–Trump tunnel between Russia and Alaska proposed yesterday “interesting.” Zelensky is “not happy with this idea.”

A Warsaw court has defied Berlin’s extradition bid for a Ukrainian suspect in the Nord Stream sabotage case and ordered his release Read Full Article at RT.com

A Warsaw court has refused to extradite a Ukrainian suspect wanted by Berlin over the 2022 pipeline blasts

A Polish court has refused to extradite a Ukrainian suspect in the Nord Stream sabotage case to Germany, ordering his immediate release and ruling that the alleged actions can be seen as “rational and just” in the context of war.

The two Nord Stream pipelines, built to carry Russian gas to Germany under the Baltic Sea, were damaged in a sabotage attack in September 2022. German prosecutors have attributed the explosions to a small group of Ukrainian nationals, including a diving instructor, Vladimir Zhuravlyov, who was detained by the Polish authorities last month under a European arrest warrant. Berlin’s previous request for his arrest was reportedly obstructed by the Polish government in 2024.

On Friday, Polish media reported the Warsaw District Court found Germany’s extradition request “unfounded,” citing a lack of evidence linking Zhuravlyov to the sabotage.

“Blowing up critical infrastructure during a war – during a just, defensive war – is not sabotage but denotes a military action,” Judge Dariusz Lubowski said. “These actions were not illegal – on the contrary, they were justified, rational and just,” he added.

Lubowski also ruled that Germany lacks jurisdiction, as the explosions occurred in international waters. The decision may still be subject to appeal.

The German investigation has led to the arrest of another suspect, former military officer Sergey Kuznetsov, detained in Italy in August. Prosecutors allege that he coordinated a team that rented a yacht and planted explosives on the pipelines using commercial diving gear.

Moscow has rejected Berlin’s version, dismissing the claim that a small group of Ukrainians carried out the sabotage as “ridiculous.”

Russian President Vladimir Putin suggested the US likely orchestrated the operation.

Warsaw, which has been one of Kiev’s staunchest backers since 2022, allegedly considered granting asylum to the suspect, according to a September report by Polish newspaper Rzeczpospolita. Foreign Minister Radoslaw Sikorski has also said he is ready to do so.

Polish Prime Minister Donald Tusk, who earlier opposed extraditing Zhuravlyov, praised the ruling, writing on social media “The case is closed.”

The Bizarre Bankruptcy At The Heart Of This Week's Regional Bank Meltdown

As we highlighted in our regional bank meltdown summary post, there was a common theme between the two banks that got hammered yesterday, ZION and WAL: a single bankrupt counterparty that led to bad debt impairments at both banks. Now, thanks to Bloomberg, we can identify who that counterparty was.

According to BBG, the bad loans reported by Zions Bancorp and Western Alliance Bancorp can be traced back to the bankruptcy of one commercial real estate investment firm in Southern California earlier this year. In the lawsuit filed on Wednesday - which also spooked investors and sent the stock plunging - Zions listed 16 addresses of properties pledged as collateral to more than $60 million loaned to an investor group. And when the Newport Beach, California-based real estate firm MOM CA Investco LLC filed for bankruptcy in February, six of those properties were listed as investments.

So what happened with the loans?

Well, as Bloomberg reports, back in 2016 and 2017, when bankers at Zions subsidiary California Bank & Trust underwrote the loans they made sure the usual cushion to protect the lender was in the contract: Zions should be first in line for repayment should the borrower default and liquidate its assets, according to this week’s complaint, filed in LA County Superior Court against defendants including Gerald Marcil, Andrew Stupin and Deba Shyam.

But two things went wrong simultaneously. First, MOM CA Investco filed for bankruptcy protection, leading to a planned sale of some its properties. Second, it turned out that, for those buildings that served as collateral for the loans Zions issued, other firms actually were ahead in line of the Salt Lake City-based bank to be paid should the real estate be liquidated.

A similar situation hit Western Alliance. The Phoenix-based bank sued an investor group including Marcil and Stupin, claimed they manipulated loan structures in a way that wrongly stopped the lender from receiving debt repayments before anyone else.

Western Alliance said the investor group still owes it more than $98.6 million. Those loans were meant to be secured by real estate in Stupin and Marcil’s investment funds, but the properties were already in foreclosure, which wasn’t disclosed to the bank, according to a complaint filed in August in Los Angeles.

In response, Marcil and Stupin's lawyer said in a statement that "my clients vehemently deny all the allegations of wrongdoing... These claims are unfounded and misrepresent the facts. We are confident that once all the evidence is presented, our clients will be fully vindicated.”

Digging deeper we find that behind the bankruptcy of MOM CA Investco is a group of Southern California commercial real estate investors who were friends before they became foes in court. The firm’s portfolio included a hotel in the exclusive enclave of Laguna Beach and an apartment complex worth $65 million in the town of Redlands, according to the February bankruptcy filing.

The MOM CA Chapter 11 was dismissed in August. In the weeks leading up to the dismissal, the federal judge overseeing the case warned the property investors that the inability to get a deal wasn’t in their interest. And throwing the case out of bankruptcy, said US Bankruptcy Judge Brendan Shannon said, wasn’t the best option.

That’s because, once the case was over, creditors would be free to file actions in state court to try seize various properties and sell them at fire-sale prices. After several court hearings in which the two main players in the real estate empire remained at odds, Shannon dismissed the Chapter 11.

Mohammad Honarkar and Mahender Makhijani founded MOM CA Investco in 2021 as a joint venture. At the time, Honarkar also ran a business selling mobile phones, while Makhijani acquired and managed distressed real estate for investors through an entity called Continuum Analytics. Among the largest investors in Continuum were Marcil and Stupin, and its legal owner is Shyam.

But the partnership soon went south, with Honarkar accusing his partners, who controlled the company, of fraud. At one point during their dispute, Makhijani used armed guards to take over some of the properties, and hired mobile billboards to drive around Laguna Beach displaying pictures of Honarkar and accusing him and two city employees of corruption, according to court filings.

It gets even more bizarre: the investors sued by Zions and Western Alliance, Marcil, Stupin and Shyam, have additional ties to a variety of investment vehicles linked to Makhijani, court filings show. The three were among the founding investors of Nano Banc, for which Makhijani is one of the largest referral sources.

Nano Banc had loaned the founders more than $100 million, according to a March arbitration filing. And Zions found that for one property it had a first lien on, a building in Laguna Beach, the deeds were assigned to Nano Banc.

And the piece de resistance: another asset, an apartment complex in Bellflower, had a deed assigned to the other bank suing the investors: Western Alliance.

In short: unprecedented chaos... but it wasn't just a busted bankruptcy and potential fraud on behalf of a shady investor group. It was also a bizarre absolute priority rule waterfall shitshow, in which nobody knew whose claims were subordinated or priority, and the result was a free-for-call collateral grab which was not quite rehypothecation, but was very close, and the result is that the secured lenders - Zions and Western Alliance - have now ended up chasing the assets pledged to their loans in court as the assets are, as the South Park cartoon puts it so well, gone... all gone.

The good news is that we now know what happened in this particular case. The question now is why did the banks not figure all of this ahead of time, and more importantly, how many more such instances of a manged absolute priority rule are there?

The US needs Tomahawk cruise missiles to be ready for national defense instead of sending them to Ukraine, the president has said Read Full Article at RT.com

Washington needs “a lot” of arms that it has been providing Kiev throughout its conflict with Russia, the president has said

It would not be “easy” for Washington to give Kiev Tomahawk cruise missiles, as the US needs them for its own protection, US President Donald Trump has said.

During a bilateral lunch alongside Ukraine’s Vladimir Zelensky before their official meeting in the White House on Friday, Trump acknowledged that the US would face certain difficulties if it were to send missiles to Kiev and found itself in a conflict of its own.

“That’s a problem. We need Tomahawks and we need a lot of other things that we’ve been sending over the last four years to Ukraine… We gave them a lot," he said.

“It’s not easy for us to give. You’re talking about massive numbers of very powerful weapons,” he added.

Trump acknowledged that allowing Kiev to conduct strikes deep into Russia could lead to “an escalation,” adding, though, that he and Zelensky would discuss the topic. Tomahawks are “an amazing weapon,” he added.

“But they’re a very dangerous weapon… It could mean a lot of bad things can happen,” Trump noted.

Trump earlier stated that he would discuss his call on Thursday with Russian President Vladimir Putin with Zelensky.

The Russian president told Trump that supplying Ukraine with the long-range missiles would not alter the course of the conflict, yet still harm relations between Moscow and Washington, according to Kremlin aide Yury Ushakov.

It would also “severely undermine the prospects of a peaceful settlement,” Putin said, according to his aide.

Tomahawks, which have a maximum range of 2,500 kilometers (1,550 miles), would be capable of reaching Moscow and cities beyond, if launched from Ukraine.

Trump is not expected to commit to supplies of the weapons, CNN wrote on Friday, citing two anonymous sources. The outlet, however, did not rule out that the president could change his mind during the talks.

President Donald Trump on Oct. 16 refiled his $15 billion defamation lawsuit against The New York Times, book publisher Penguin Random House, and three NY Times reporters after a judge’s earlier rejection of the case.

In a 40-page amended complaint, Trump accused the defendants of defamation over two articles and a book published last year ahead of the presidential election, alleging they contained statements intended to “wrongly defame and disparage” his professional reputation.

The lawsuit named NY Times reporters Susanne Craig and Russ Buettner, as well as NY Times chief White House correspondent Peter Baker, among the defendants.

According to the filing, among the alleged defamatory statements are claims that Trump received more than $400 million from his father through “fraudulent tax evasion schemes.” The complaint also cited The New York Times’s coverage of his role in the TV series “The Apprentice” and its statements about his compliance with federal tax laws.

“Defendants individually and collectively published numerous false, malicious, and defamatory statements while realizing that these statements were false, or, at a minimum, with reckless disregard for the truth,” the lawsuit reads.

Trump is seeking $15 billion in compensatory damages—consistent with his original suit filed on Sept. 15—and an unspecified amount of punitive damages, which will be determined upon trial.

The Epoch Times reached out to The New York Times and Penguin Random House for comment, but did not receive a response by publication time.

U.S. District Judge Steven Merryday previously tossed the original complaint due to its length, saying that it “stands unmistakably and inexcusably athwart the requirements of Rule 8” of the Federal Rules of Civil Procedure. The judge then gave Trump 28 days to amend the lawsuit.

The first complaint amounted to 85 pages.

A spokesperson for The New York Times previously told The Epoch Times that Trump’s lawsuit was meritless and called it an attempt by the president to “stifle and discourage independent reporting.”

In a Truth Social post announcing the initial filing on Sept. 15, Trump said The New York Times was “a virtual mouthpiece for the radical left Democrat Party,” citing its endorsement of then-Democratic presidential candidate and Vice President Kamala Harris during the 2024 presidential election.

“The New York Times has been allowed to freely lie, smear, and defame me for far too long, and that stops, NOW,” the president said in his post.

Trump also filed a lawsuit against Paramount over CBS’s “60 Minutes” interview with Harris, alleging that CBS edited the interview to benefit Harris in the election. Paramount paid $16 million to settle the lawsuit. Trump said in July that he anticipated another $20 million from Paramount’s “new owners,” which he said would come in the form of “advertising, PSAs [public service announcements], or similar programming.”

"Literally Never Had A Job": Highlights From Fiery NYC Mayoral Debate As Cuomo, Sliwa Bash Socialist Candidate's Record

New York City mayoral candidates Democratic nominee Zohran Mamdani, his primary opponent Andrew Cuomo, and Republican nominee Curtis Sliwa squared off on Oct. 16 in a bid for the seat that current Mayor Eric Adams is vacating in 2026.

Adams dropped out of the race on Sept. 28.

The debate, co-hosted by POLITICO, NBC 4 New York, and Telemundo 47, took place at 30 Rockefeller Center in Manhattan.

Socialist New York City mayoral candidate Zohran Mamdani denies being a "communist," yet his limited job track record and history of promoting Marxist ideology raise alarm bells. He has long pushed nation-destroying policies, echoing the globalist agenda pushed by dark-money-billionaire-funded NGOs such as all things 'woke', and of course, the “defund the police” movement, made famous by the Marxist rioters BLM that helped trigger a nationwide crime wave in recent years. That’s one of the key reasons President Trump has deployed federal officers and National Guard members to certain progressive cities plagued by out-of-control crime because of police shortages.

And yet, after left-wing Democrats pushed toxic social and criminal justice reforms that sparked nothing but chaos, the democratic socialist still has strong odds of becoming the next mayor of New York City.

During the debate, Mamdani appeared to backtrack on his position about Hamas laying down their arms, saying, "Of course I believe that they should lay down their arms."

Mamdani was responding to a question from a moderator who said his previous answer, which was made to Fox News anchor Martha MacCallum, was "confusing," after he dodged questions when she asked if he believes Hamas should lay down their weapons and leave leadership in Gaza, according to the cease-fire agreement they entered into.

"I'm proud to be one of the first elected officials in the state who called for a ceasefire," Mamdani said.

"That means all parties have to ceasefire and put down their weapons. And the reason that we call for that is not only for the end of the genocide, but also an unimpeded access of humanitarian aid. I, like many New Yorkers, and I'm hopeful that this ceasefire will hold."

Mamdani was also pressed by Cuomo on his refusal to condemn the phrases "from the river to the sea" and "globalize the intifada," both of which are widely seen as calls for the extermination of Jews. Sliwa pressed on this issue as well, telling Mamdani, "Jews don't trust that you will be there for them when they are victims of antisemitic attacks."

Mamdani answered that he will be a mayor for all New Yorkers, saying, "Jewish New Yorkers who have told me about their fear in living in this city, and I will be a mayor who finally addresses that, not through the theatrics of the politics on the stage, but through action."

2. National Guard not welcome

President Donald Trump’s deployment of National Guard troops to major American cities also loomed large over Thursday night’s New York City mayoral debate.

Candidates were asked about the "threat hanging over the city" of National Guard troops being sent to New York City. All three candidates indicated they would oppose troops being sent to the city.

Mamdani asserted that "What New Yorkers need is a mayor who can stand up to Donald Trump and actually deliver on that safety."

"When Donald Trump sent ICE agents on people in Los Angeles, Andrew Cuomo said that New Yorkers need not overreact. That is the furthest answer that New Yorkers are looking for. They are looking for someone who will lead, someone who will say that they will have their back, someone who will actually fight for the people of this city," said Mamdani.

Cuomo, meanwhile, said that "the answer in the subways is not more National Guard" but rather "more NYPD is the answer."

3. ‘Literally has never had a job’

Cuomo attacked Mamdani’s thin resume, saying, "He has no experience."

"This is not a job for someone who has no management experience, to run around 300,000 people, no financial experience to run a $115 billion budget," said the former governor.

"He literally has never had a job. On his resume, it says he interned for his mother. This is not a job for a first timer. Any day you could have a hurricane, God forbid, a 9-11, a health pandemic, if you don't know what you’re doing, people will die."

Mamdani immediately shot back, "If we have a health pandemic, then why would New Yorkers turn to the governor who sent seniors to their death in nursing homes? That’s the kind of experience that’s on offer here today."

"What I don’t have in experience I make up for in integrity, and what you don’t have in integrity you could never make up for in experience," he added.

Cuomo dismissed the nursing homes dig as a political investigation that "went nowhere."

4. Defund the police continues to haunt Mamdani

Cuomo also knocked Mamdani for previous calls to defund the police and statements denouncing law enforcement.

"Respect the police. They’re not racists as the assemblyman calls them, they’re not a threat to public safety as he says, they’re not anti-queer, they are here to protect New Yorkers, work with them, fortify them," said Cuomo.

Sliwa jumped in at this moment to deliver a jab to Cuomo, saying, "That’s ironic that you say that now … your parole board released 43 cop killers back into the street. Your father, when he was governor, released none. I knew Mario Cuomo; you’re no Mario Cuomo."

In response to Cuomo’s attack, Mamdani said, "As much as Andrew Cuomo wants to bring up tweets from 2020, which is around the same time that he was sending seniors to their death in nursing homes, I am looking to work with police officers, not to defund the NYPD."

Mamdani again touted his plan to have "dedicated teams of mental health outreach workers" deployed to the top 100 subway stations with the highest levels of mental health crises and homelessness.

5. No love for Hochul

In a debate filled with candidates interjecting and talking over each other constantly, the room suddenly went silent when a moderator asked, "Show of hands. Who supports [New York Gov.] Kathy Hochul for re-election?"

Not a single candidate raised their hand.

Cuomo, who picked Hochul as his lieutenant governor, said, "We have to know who’s running."

Mamdani said, "It’s a decision that should be made after this general election."

He noted, however, that he believes Hochul is "doing a good job, and not only delivering for New Yorkers but also standing up to Donald Trump."

"Then endorse her!" Cuomo interjected. "Why don’t you endorse her?"

Mamdani noted, "I appreciate her support, and I appreciate her work," but said, "I’m focusing on November."

Sliwa signaled his support for the gubernatorial campaign of Rep. Elise Stefanik, R-N.Y., saying, "a Republican Mayor Curtis, a Republican Governor Stefanik … save this city."

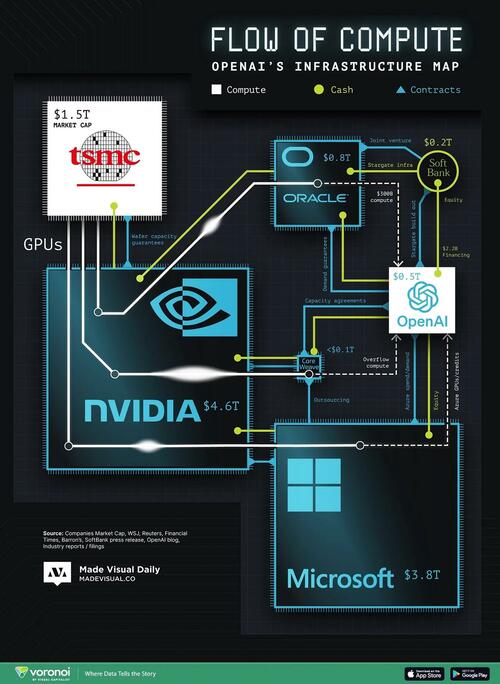

Visualizing The Compute, Cash, & Contracts That Power OpenAI

In order to train and deploy cutting-edge AI models like ChatGPT, OpenAI relies on a sprawling infrastructure network involving multiple billion-dollar entities, intricate contracts, and vast capital commitments. A new visualization from Made Visual Daily maps this infrastructure pipeline using three flows—compute, cash, and contracts—highlighting the increasingly circular nature of AI development funding.

The map, via VisualCapitalist.com, synthesizes data from public financial reports, media disclosures, and filings in an attempt to show who builds what, who pays whom, and where potential risk may be accumulating in the system.

The biggest nodes in the diagram are familiar names: Nvidia ($4.6 trillion), Microsoft ($3.8 trillion), TSMC ($1.5 trillion), and Oracle ($0.8 trillion).

OpenAI itself, valued at around $500B in its most recent secondary sale, anchors the middle of the chart. Microsoft, in particular, plays a dual role—both providing compute (via Azure) and injecting capital and GPU credits back into OpenAI.

The GPU Supply Chain: Scarcity, Dominance, and Dependency

The engine behind OpenAI—and much of today’s generative AI—is the Nvidia GPU.

But these chips don’t come out of thin air. The GPU supply chain is global and fragile:

Design: Nvidia designs the chips in-house.

Fabrication: TSMC (Taiwan Semiconductor Manufacturing Company) fabricates the chips at its advanced 5nm and 4nm nodes.

Assembly: The chips are then packaged and tested by firms like Quanta and Foxconn.

Deployment: Server makers such as Supermicro integrate them into AI-optimized racks and clusters.

Delivery: These clusters are shipped to cloud providers like Microsoft Azure and CoreWeave.

Any disruption along this chain—whether geopolitical, economic, or logistical—can send shockwaves through the entire AI sector. That’s why the U.S. has placed tight export controls on AI chips, and why countries like China are scrambling to develop domestic alternatives.

Demand for H100s has grown so intense that cloud firms and startups alike are reserving capacity months or even years in advance. In rare cases, some even use GPUs as collateral to secure financing, reinforcing their role as a new strategic commodity.

Closed-Loop Capital and the AI Bubble Risk

What makes the modern AI ecosystem remarkable isn’t just the number of players involved—it’s how deeply interwoven their financial and operational relationships have become.

Microsoft, for instance, has invested over $13 billion in OpenAI, while also serving as its primary cloud and compute partner through Azure. Much of OpenAI’s model training runs on clusters powered by Nvidia GPUs, procured via Microsoft’s cloud infrastructure.

At the same time, Microsoft is the primary customer of CoreWeave, a rapidly growing cloud provider that also buys large volumes of Nvidia hardware—often financed through credit arrangements with private investors and funds.

This creates an interdependent web of capital, compute, and contracts, where the same dollars and chips circulate between a handful of firms dominating AI’s supply chain. Analysts have noted that such tight coupling could magnify shocks if demand or funding conditions change abruptly.

To dig deeper into the relationship between OpenAI and its backers, explore our related post: OpenAI vs Big Tech.

Zelensky Desperately Pitches Drones For Tomahawks At White House

Update(1542ET): In a somewhat lengthy Q&A with the press, Presidents Trump and Zelensky fielded a variety of questions before starting a closed-door meeting at the White House, with each leader's full delegations present.

All eyes have been on the potential decision to transfer Tomahawks to Ukraine, but President Trump at every turn dodged the question, and did not offer anything clear on Tomahawks one way or the other. But he did say at one point when asked about concerns over the Pentagon's own dwindling missile stockpiles that "I have to make sure we're stocked up as a country."

That opened up an interesting moment where Zelensky offered "thousands" of Ukrainian drones in exchange for receiving Tomahawks, though Trump appeared cool toward the idea, and noted that the United States already possesses excellent and cutting-edge drone production. The moment unfolded below:

BREAKING: Just as Trump says "hopefully they won't need Tomahawks," Zelenskyy chimes in and begs for them and wants to trade for Ukrainian drones.

Zelenskyy isn't so focused on peace today.

President Trump is LASER FOCUSED: "We would much rather have the war be over." pic.twitter.com/U4h2pWwvYw

Just ahead of Ukraine's Zelensky arriving at the White House to meet with President Trump, Russia announced Friday morning that its forces had seized three more villages in Ukraine’s Dnipropetrovsk and Kharkiv regions.

Russian troops captured Pishchane and Tykhe in Kharkiv and Pryvillia in Dnipropetrovsk, the Kremlin said. The development in the Kharkiv region is going be met with particular alarm among Kiev's backers in the West, given that the Ukrainian's military's 2022 counteroffensive had actually retaken much of Kharkiv.

But the Russian military is clearly pushing forward again, and is eyeing the capture of Kupiansk next, which is a crucial logistics hub in the region.

Russia's military command has at the same time tallied its forces have captured eight Ukrainian settlements in total over the course of the past week.

A statement in TASS says "In the Kharkov direction, Battlegroup North units liberated the settlement of Tikhoye in the Kharkov Region through decisive operations... Battlegroup West units liberated the settlements of Borovskaya Andreyevka and Peschanoye in the Kharkov Region in decisive operations...battlegroup Center units liberated the settlements of Moskovskoye, Balagan and Novopavlovka in the Donetsk People’s Republic through active and decisive operations."

The Defense Ministry continued listing out: "Over the past week, Battlegroup East units liberated the settlements of Alekseyevka and Privolye in the Dnepropetrovsk Region," it said.

Without doubt, Moscow has timed its "announcement" touting the capture of all these locations to correspond with Zelensky's visit to Washington, also coming after Thursday's Trump-Putin phone call.

The only 'leverage' that Ukraine might have is related to its stepped-up long-range drone offensive which has wreaked havoc on Russian oil.

Nobody waited for Zelensky in Washington. So, his PR crew organised a stunt.

They lined up Jermak, the head of Zelensky’s Presidential Office and the pilots of the plane.

The PR female introduces Jermak as if Zelensky did not know his comedy ex-manager.pic.twitter.com/NYFqTz95Q4

Depot after depot has been hit over the past weeks and months, including also vital oil shipping terminals on the Crimean coast. If Ukraine received long-range missiles from the West and the United States, it will certainly train them on such vital targets.

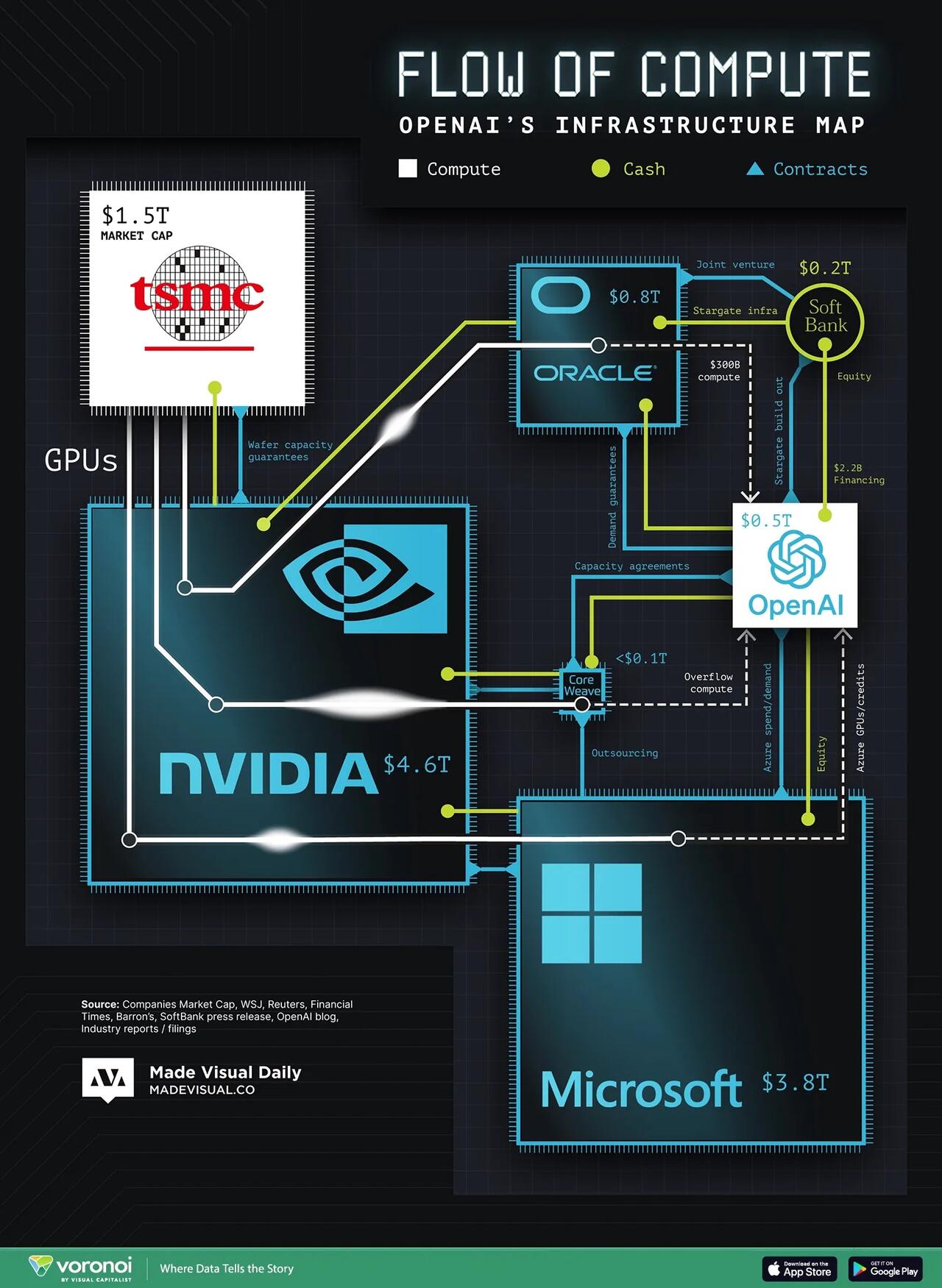

"Once upon a time, a learned man watched his friends grow rich by investing in a company that promised to revolutionise trade. Attracted by the prospect of easy riches, he joined the party, but was cautious at first, investing only small amounts. He even sold his shares for a tidy profit when he felt their price could no longer be rationally justified.

But, as the mania grew and the share prices kept increasing, he couldn’t resist… he bought back in, this time with more money, more conviction, and more confidence.

The bubble popped. He lost a fortune. The man was so shaken that he declared he could ‘calculate the motions of the heavenly bodies, but not the madness of people."

This story of Sir Isaac Newton and the South Sea Bubble of 1720 offers a cautionary tale about speculative excess, even among the most brilliant minds.

But why is it so difficult, even for one of the smartest people ever to have lived, to resist the lure of financial bubbles?

Human nature fuels the hype

During periods market exuberance, it’s not just valuations that defy gravity, so does reason. As Keynes famously put it, ‘It is better for reputation to fail conventionally than to succeed unconventionally’. In other words, it’s easier to join the crowd and be wrong together than to stand alone and be right too early.

For example, during the dot-com boom, financial news channels gave extensive coverage to IPOs, reflecting the excitement of the time.. Analysts who dared to question valuations were labelled ‘out of touch’.

Fund managers and analysts are human too – reading the same headlines, hearing the same chatter, and many will feel the same level of Fear Of Missing Out (FOMO). When everyone else is riding the rocket ship, sitting on the launchpad with a sceptical look and a clipboard isn’t just lonely, it can be career-threatening.

The bubble becomes a social phenomenon, not just a financial one.

Betting against a bubble is structurally hard

Even if a fund manager has the courage to go against the grain, the tools to do so are hardly user-friendly. Going long is simple: buy, hold, and enjoy the ride. Going short? That’s a different beast.

Shorting equities means borrowing stock, posting margin, and paying dividends to the lender. If the stock keeps rising, margin calls pile up. In fixed income, shorting often involves paying the bond’s coupon out of pocket; negative carry at its finest. All the while, the bubble may continue expanding while others enjoy a windfall .

As Keynes (again) warned, ‘markets can remain irrational longer than you can remain solvent’. And irrational markets tend to be very, very solvent.

Short sellers during the meme stock episode faced significant challenges, highlighting the risks of contrarian positioning in volatile markets. Hedge funds betting against GameStop found themselves squeezed by retail traders armed with Reddit threads and stimulus cheques. The stock soared, losses mounted, and some funds were forced to close positions at eye-watering losses. It was a masterclass in how expensive it can be to be right too early, and a reminder that the market doesn’t always reward rationality.

Contrarians need saintly patience (and patient saints)

To survive a bubble, a contrarian needs not just conviction, but also investors who are aligned with a long-term philosophy and understand the nature of contrarian strategies. Take Warren Buffett in the late 1990s. While dot-com darlings soared, Buffett stuck to his guns; no tech, no hype, just fundamentals. Critics said he didn’t ‘get it’. His returns lagged, but his investors stayed loyal.

When the bubble burst in 2000, Buffett emerged unscathed, vindicated, and wealthier. His story is a reminder that sometimes the tortoise really does beat the hare, if the tortoise has patient shareholders.

Buffett’s success wasn’t just about his investment philosophy, it was about the trust he had built with his investors over decades. They understood that his approach was long-term, even if the market wasn’t. Compared to investor that are more reactive to short-term performance , Buffett’s investor base acted more like partners than clients. That kind of long-term perspective is invaluable when swimming against the tide.

Source: Bloomberg

All told, the contrarian’s road can be lonely and often met with scepticism. You not only have to be right about the endgame, but also have to stay invested long enough to enjoy it. As one market wit quipped, contrarian investing can feel like ‘standing in front of an oncoming train and mumbling, ‘it will stop…’

History shows us that overheated markets cool down – bubbles tend to burst – but often not before testing the resolve of those who challenge prevailing market sentiment. Yet for the fund managers who can resist the rally, deploy the right tools, and manage patient capital, the rewards of contrarian courage can be substantial.

Going against the crowd in a bubble isn’t just a test of conviction, it’s an opportunity to shine when the dust finally settles.

The US Department of War has accused Netflix of feeding “woke garbage to their audience and children” over a new gay military show Read Full Article at RT.com

Army standards are “uniform and sex neutral,” a spokeswoman for the department of war has said

The Pentagon has accused Netflix of producing “woke garbage,” over the streaming service’s latest show centered around a gay man joining the US Marines. The series premiered amid a campaign by President Donald Trump and Secretary of War Pete Hegseth to end “woke culture” in the military.

US Department of War spokeswoman, Kingsley Wilson, told Entertainment Weekly, it does not support Netflix’s “ideological agenda.” The US military “will not compromise our standards, unlike Netflix whose leadership consistently produces and feeds woke garbage to their audience and children,” Kingsley said, adding that the Pentagon is currently focused on “restoring the warrior ethos.”

“Our standards across the board are elite, uniform, and sex neutral because the weight of a rucksack or a human being doesn't care if you're a man, a woman, gay, or straight,” the spokeswoman stated.

Last month, Hegseth announced new personnel standards for the military, insisting on “male-level” fitness requirements to be able to face “life and death” situations on the battlefield. “Standards must be uniform, gender-neutral, and high. If not, they’re not standards,” he said at the time, arguing that any other approach would “get our sons and daughters killed.”

Back in February, the secretary of war also dismissed the motto “diversity is our strength” as the “dumbest” in military history. The Pentagon has faced recruitment shortages for years. 2023 marked the military’s deepest recruitment gap – of 15,000 – since the abolishing of the draft in 1973, according to a June report.

Republican lawmakers have previously blamed the problem on the department’s prioritization of diversity over military readiness, which allegedly drove would-be recruits away. A 2021 report commissioned by Republicans on the Senate Armed Services Committee found that the US Navy was focusing more on “wokeness” and diversity than winning wars.

Netflix has not responded to the Entertainment Weekly’s request for comment.

Auto Loan Delinquencies Surge 50% As Cracks Deepen Across U.S. Credit Markets

A month after bankruptcies of subprime auto lender Tricolor and auto-parts supplier First Brands, new cracks emerged in U.S. credit markets. This week, Zions and Western Alliance disclosed they were victims of loan fraud tied to funds investing in distressed commercial real estate. The revelations come amid broader credit trouble, and shifting our focus back to autos, there's new data this morning about credit products tied to the riskiest consumers that have seen a 50% surge in delinquencies.

Bloomberg cites data from the credit-scoring company, VantageScore, which reveals that delinquencies among the low-tier consumers have surged 50% since 2010. Fueling the delinquencies is a perfect storm of record-high car prices, elevated interest rates, longer loan terms, and monthly payments that average nearly as much as rent for some folks.

Since 2019, new vehicle prices have jumped over 25% to $50,000, while average monthly payments reached $767, with 20% of borrowers paying over $1,000 per month. Loan rates now exceed 9%, worsening the affordability crisis.

Notably, prime and near-prime borrowers are now defaulting faster than subprime consumers, as lenders tightened standards for the lowest-credit segment, according to the report. The average auto loan balance has risen 57% since 2010, and many borrowers are "upside-down", owing more than their cars are worth.

"We're seeing the cost of cars and the cost related to car ownership increase enormously," VantageScore chief economist Rikard Bandebo said in an interview. "In the past five years, it has increased even faster."

Bandebo continued, "That's a double... You've been hit by the increased cost of the car and then the financing cost of the car."

"Consumers now are in a more precarious position than they've been since the last recession," Bandebo said. "We've seen this growing trend over the last several years of more and more consumers struggling to make ends meet, and it's looking like that trend is going to continue into next year."

Here's the sequence of alarming events unfolding in the credit markets in recent weeks:

UBS analyst Jolie Ho commented on the credit market cracks:

Two U.S. regional banks, Zions and Western Alliance, said they were the victims of fraud on loans to funds that invest in distressed commercial mortgages, fueling concern that more cracks are emerging in the credit markets. Zions sank 13% on Thursday after it disclosed a $50 mn charge-off for a loan underwritten by its wholly-owned subsidiary. Western Alliance shed almost 11% after it said it made loans to the same borrowers. Bloomberg reported that the disclosures add to recent loan blowups, including bankruptcies at subprime auto lender Tricolor and auto-parts supplier First Brands. JPMorgan and Fifth Third reported hundreds of millions in combined losses tied to Tricolor, while Jefferies revealed exposure to First Brands. While these hits can be easily absorbed by the biggest U.S. banks, the totals are worrisome for regional lenders. U.S. credit-risk gauges worsened on Thursday, with the spread on the Markit CDX North American Investment Grade Index widened as much as 1.69bp to 54.47, as reported. A similar gauge for junk bonds, which falls as credit risk climbs, dropped as much as 0.49 point to 106.87.

Meanwhile, rate traders have priced in two 25 bps cuts by year's end.

Let's not forget about the government shutdown... All is troubling.

US President Donald Trump has acknowledged that allowing Ukraine to conduct strikes deep into Russia would be an escalation Read Full Article at RT.com

The US president has acknowledged that allowing Ukraine to conduct strikes deep into Russia would be an escalation

US President Donald Trump and Ukraine’s Vladimir Zelensky have begun talks at the White House. The meeting is taking place after Trump held a phone call with Russian President Vladimir Putin on Thursday, in which the two leaders agreed to have a summit meeting in Budapest, Hungary.

The Ukrainian leader arrived in Washington on Friday at the head of a large delegation. After welcoming Zelensky, Trump told reporters that his call with Putin will be high on the agenda: “We had a big call yesterday, as you know, with President Putin, and we’ll be talking about it.”

Trump added that the two will discuss providing Ukraine with new weapons, while acknowledging that this could escalate the conflict.

“We’re going to be talking about that… It’s an escalation, but we’ll be talking about that,” he said.

Zelensky earlier asked Trump to supply Kiev with Tomahawk cruise missiles capable of striking targets up to 2,500 kilometers (1,550 miles) away, meaning they could potentially reach Moscow and far beyond.

Russia earlier warned that supplying Tomahawks would “not change the situation on the battlefield,” but would “severely undermine the prospects of a peaceful settlement” and harm US-Russia relations.

Pivoting to a potential dialogue to end the conflict, Trump said there is a lot of “bad blood” between Putin and Zelensky, and this is holding up a settlement. He added that the Budapest summit would most likely be a “double meeting,” with Zelensky being in touch.

“[Putin] wants to get it [conflict] ended. President Zelensky wants it ended. Now we have to get it done,” Trump said.

Zelensky accused the Russian president of not wanting a ceasefire, adding that his goal in the negotiations with Trump is “to get what we need to push Putin” to negotiate. According to Zelensky, Ukraine is also seeking robust security guarantees. “NATO is the best, but weapon[s] [are] very important.”

Russia has denounced the Western weapons shipments to Ukraine, warning that they only prolong the conflict. It is also strongly opposed to Kiev’s bid to join NATO, describing it as one of the key reasons for the conflict.

Federal regulators will no longer require banks to spell out how they manage climate-related financial risk, following objections from officials in the Trump administration and Republican lawmakers, who said that climate policy was distorting financial regulation.

In a joint move announced on Oct. 16, the Federal Reserve, the Federal Deposit Insurance Corporation, and the Office of the Comptroller of the Currency rescinded a set of rules called the Principles for Climate-Related Financial Risk Management for Large Financial Institutions.

Introduced in 2023, the rules applied to banks with more than $100 billion in assets and were intended to incentivize institutions to integrate climate considerations into governance, scenario analysis, and risk oversight.

Regulators said the withdrawal reflects a return to long-standing safety and soundness standards that already require banks to manage all material risks—without singling out climate.

“The agencies do not believe principles for managing climate-related financial risk are necessary,” the notice stated, while a Federal Reserve memo further clarified that such guidance risked distracting banks from focusing on core vulnerabilities such as credit, liquidity, and operational risk.

“Existing safety and soundness standards require large financial institutions to have effective risk management processes commensurate with the size, complexity and risk of their activities,” the memo stated, adding that existing rules and guidelines “are sufficient to help ensure financial institutions are managing all material risks.”

Fed Governor Christopher Waller welcomed the move with a two-word statement: “Good riddance.”

Michelle Bowman, the Federal Reserve’s vice chair for supervision, also backed the rollback, saying in a statement that the climate framework had created “confusion about supervisory expectations” and imposed compliance costs and burdens without improving financial stability. She said banks should focus on “core risks” such as credit and liquidity rather than speculative long-term climate scenarios, and that the rules could reduce credit supply and raise borrowing costs for American households.

“One likely potential consequence could be to discourage banks from lending and providing financial services to certain industries, forcing them to seek credit outside of the banking system from non-bank lenders,” Bowman said. “This could result in decreasing or eliminating access to financial services and increasing the cost of credit to these industries. These costs will ultimately be borne by consumers.”

But the decision drew dissent from several other Fed officials. Federal Reserve Governor Michael Barr called the rescission “short-sighted” and said it would “make the financial system riskier even as climate-related financial risks grow.” He pointed to recent disasters such as Hurricane Helene and the California wildfires as evidence of mounting financial exposure.

“The rescission contains literally no evidence to support taking this step only two years after putting the principles into effect,” Barr said. “We owe the public a rational, evidence-based explanation for our actions, and this rescission fails that test.”

Federal Reserve Governor Lisa Cook, while accepting the board’s decision and noting the benefit of regulations that are clear and predictable, said that she expects banks to remain vigilant in assessing severe weather risks.

“My view has not changed since 2023: to the extent severe weather events could cause disruptions to specific firms or to the financial system, I would expect that large banks would seek to be proactive in monitoring, assessing, and appropriately addressing such risks,” Cook said. “I also believe it is advantageous for the banking industry to have stable, well-understood supervisory expectations.”

The rollback marks a broader effort by the Trump administration to unwind climate-related directives across financial agencies and limit the role of environmental, social, and governance factors in regulatory supervision.

That shift has extended beyond the banking regulators. In September, the U.S. Financial Stability Oversight Council, chaired by Treasury Secretary Scott Bessent, voted to disband two panels dedicated to analyzing climate-related systemic risks. Bessent said the decision was a necessary refocus on “core financial stability issues,” including bank safety, liquidity risks, and oversight of nonbank financial firms.

Climate advocates called the move a setback for efforts to prepare the financial system for extreme weather disruptions.

An Ofcom investigation found the BBC to be “materially misleading” in its ‘Gaza: How to Survive a Warzone’ documentary Read Full Article at RT.com

An Ofcom investigation found the British state broadcaster to have been “materially misleading” in a documentary film on Gaza earlier this year

British communications watchdog Ofcom has ruled that state broadcaster the BBC breached journalistic code for failing to disclose that the narrator of a Gaza documentary was the son of a Hamas official.

In a statement on Friday, the regulator announced that its probe into the BBC’s ‘Gaza: How to Survive a Warzone’ documentary found it to be “materially misleading.”

The film, which was originally released in February, was partly narrated by the 13-year-old son of the Hamas deputy agriculture minister. The Palestinian militant group is designated as a terrorist organization in the UK, US, and EU.

“The program’s failure to disclose that the narrator’s father held a position in the Hamas-run administration was materially misleading,” Ofcom said on Friday, adding that this could have eroded audience trust.

“This represents a serious breach of our rules,” it said.

The watchdog has directed the BBC to publish a statement on the investigation’s findings during evening primetime, with an exact date to be determined later.

The BBC apologized for the incident on Friday, and accepted the regulator’s decision.

The broadcaster has been under intense scrutiny over its coverage of the Gaza war. It has recently faced backlash for airing an anti-Israeli musical performance from Glastonbury Festival.

Last year, more than 100 staff members complained to Director General Tim Davie of insufficiently covering the Palestinian side of the conflict.

Ofcom sanctioned RT and revoked its broadcasting license over its coverage of the Ukraine conflict, soon after the escalation in 2022. RT and other Russian media outlets have faced sanctions and outright bans in many Western European nations since.

Despite this, they have expanded their reach, while Western networks have scaled back their activities amid budget cuts and shifting foreign policy concerns, the BBC reported in August.

Dear Mr. President, Americans Don't Care Who Owns Donetsk, So Why Risk WW3 By Sending Tomahawks?

Poll after poll has shown that the overwhelming majority of Americans reject direct US military involvement in Ukraine - such as sending troops or other actions which could constitute the start of direct conflict with nuclear-armed Russia.

The reality also remains that most Americans can't find Donetsk, Kherson, Luhansk and Zaporizhzhia on a map. Does the American public really want to constantly poke the Russian bear over places they can barely pronounce? Do they really care who owns the Donbass?"Where!?..." - your average Joe sixpack is likely asking.

Why then, Mr. Trump, are you actually contemplating giving Zelensky, who you once dubbed the 'greatest salesman on Earth', America's own vital long-range Tomahawk missiles?

Why are you indulging yet a fourth in-person meeting with Zelensky (and specifically his third trip to the Oval Office) since you took office in January? Where is the pressure on Zelensky to cede territory and rapidly end this bloody and tragic war? Where are the loud assurances of no more NATO expansion to Russia's border?

Why can't the Ukrainian government, which has already received billions in US taxpayer funds, so much as admit that it has lost Crimea forever? Even this smallest of admissions and concessions would be a big something offered on the path to peace. And yet Kiev remains vocally against ever ceding Crimea, despite the obviously impossibility of ever getting it back (and absolutely everyone knows this).

Instead of any semblance of the ability to make compromise, even though it's obvious to pretty much all that Ukraine's military has been steadily losing a 'war of attrition', Zelensky is busy meeting with Raytheon executives before walking into the White House on Friday morning.

This is all part of the pressure and pitch to persuade Trump to give Ukraine the sought after long-range missiles capable of reaching all main population centers in Russia.

"We discussed Raytheon's production capabilities, possible ways of our co-operation to strengthen air defence and increase Ukraine's long-range capabilities, and the prospects for Ukrainian-American production," Zelensky posted on Telegram early Friday.

Even mainstream, generally anti-Kremlin outlets like the BBC understand that this would open up a new phase in the war, where powerful American weapons are directly raining down on Russian cities:

We've been reporting that the possibility of the US sending Tomahawk missiles to Ukraine is causing "extreme concern" in the Kremlin. That's because these missiles could drastically increase Ukraine's range capabilities.

As the map below shows, Tomahawks can strike objects up to 1,600km (995 miles) away - putting dozens of Russian military bases, air defense sites and command centers in the range of fire.

There's also been much reporting saying that American contractors and personnel would have to themselves man the systems or oversee them, which is yet more 'boots on the ground' mission creep which Trump had earlier vowed to resist.

I met with representatives of the defense company Raytheon, which produces, in particular, Patriot systems.

I told them about the battlefield situation and Russia’s intensified attacks on our people and civilian infrastructure.

— Volodymyr Zelenskyy / Володимир Зеленський (@ZelenskyyUa) October 17, 2025

Again, will Washington risk WW3... all in the name of 'leverage' against Putin... while bowing down to yet another Zelensky demand - this time in the form of missiles that can reach 1,000 miles inside Russia? If roles were reversed, and a foreign entity were on our doorstep launching long-range missiles into the United States, we would without doubt immediately go to war and be put on nuclear alert.

Why risk all of this... again, for the question of who owns tiny Ukrainian oblasts halfway across the globe which most Americans could in reality care less about?

There's still hope that rational minds will prevail at the White House, based at least on some of Trump's sarcasm on display last night...

Trump:

I said to Putin: "would you mind if I gave a couple of thousand Tomahawks to your opposition? "

Below, a ZeroHedge reader and top commenter submitted this astute observation on the likely true state of things vis-a-vis Washington and Europe in the context of the Ukraine crisis.

* * *

The “Democracy vs. Autocracy” myth died in Ukraine’s trenches. What replaced it is far darker: the engineered deconstruction of Europe itself. Cheap Russian energy was severed (via Nord Stream sabotage), not to help Ukraine win — but to break Europe’s economic spine. Weapons stockpiles were drained into a black hole, and now the continent is left dependent on overpriced U.S. arms, powerless to forge its own peace.

NATO’s eastern expansion was never about defense — it was about destabilizing Russia and locking Europe into vassal status. Now, as Ukraine bleeds dry, the Empire smiles: the real target was never Moscow, but Brussels, Berlin, and Paris. This isn’t a blunder. It’s a controlled demolition.

Donald Trump has refiled a $15 billion NYT defamation suit against in Florida after a judge dismissed the original complaint Read Full Article at RT.com

The US President’s previous defamation claim against the newspaper was struck down for being “improper and impermissible”

US President Donald Trump has renewed his $15 billion defamation lawsuit against The New York Times, its reporters, and publisher Penguin Random House.

Trump initially submitted a 85-page-long lawsuit against the paper last month, accusing it of lying about him for decades and serving as a mouthpiece for the “Radical Left Democratic Party.” He claimed the outlet was “one of the worst and most degenerate newspapers in the history of our country” and described its endorsement of his Democratic rival in 2024, Kamala Harris, as “the single largest illegal campaign contribution, EVER.”

However, the original filing was dismissed as “decidedly improper and impermissible.” Judge Steven D. Merryday claimed it read more like a political attack than a legal argument and ordered Trump and his team to resubmit the complaint and make sure it does not exceed 40 pages.

The new complaint, filed on Thursday, is exactly 40 pages long and now lacks original passages on Trump’s 2024 election victory and the “Russia Collusion Hoax.” The name of a reporters listed in the original, Michael S. Schmidt, has also been dropped.

Trump’s attorneys allege that statements made in The New York Times and the 2024 book Lucky Loser, published by Penguin Random House, were “malicious, defamatory, and disparaging” toward his reputation and career achievements. The suit seeks both financial damages and formal retractions of the claims. A spokesperson for Trump’s legal team has said the president is “continuing to hold the Fake News responsible through this powerhouse lawsuit.”

New York Times spokesperson Danielle Rhoades Ha responded by saying the paper “will not be deterred by intimidation tactics.”

GDP is like collecting data on passenger satisfaction with the dessert cart on the Titanic and declaring everyone is delighted as the great "unsinkable" ship settles into the icy waters of the Atlantic.

That Gross Domestic Product (GDP) is an outdated and misleading metric of the economy is widely accepted. The problem isn't an abstraction, as we manage what we measure and so policymakers and citizens alike make decisions on what's being measured. If what's being measured is misleading, then we're flying blind.

Economist Joseph Stiglitz has long advocated for an overhaul for what we measure economically, focusing on well-being rather than adding up transactions. A new book The Measure of Progress: Counting What Really Matters, explains the difficulty of the overhaul. A recent article on the topic addressed the urgency of the task (Foreign Affairs, May/June 2025, paywalled):

"For Americans, these are tumultuous times. Inequality in income and wealth is at historically high levels. Artificial intelligence is reshaping society at an unprecedented pace, prompting layoffs and putting entire professions at risk. According to an estimate by the Brookings Institution, up to 85 percent of current workers in the U.S. labor force could see their jobs affected by today's generative AI technology. In the future, that percentage could climb even higher.

At moments of danger and uncertainty, it is usually the task of governments to protect people and help them navigate change--to step in when markets cannot. Yet Americans seem to have little belief in Washington's capabilities. Over the past two decades, public trust in the U.S. government has plummeted by 40 percent. Some Americans believe the federal government has been absent. Others believe it has failed to meet pressing challenges, including the rising cost of living, and the potential disruptions of AI. Either way, Washington has its work cut out for it as the government tries to regain Americans' trust.

So where can it start? The Measure of Progress, meanwhile, takes aim at the economic data that states use. According to Coyle, analysts evaluate the economy using outdated, limited metrics, causing policymakers to misunderstand the challenges citizens face.

Coyle's book is focused on understanding the economy as it exists today. But her argument--that analysts and governments have failed to properly measure peoples' well-being--is equally essential. The metrics that economists use, Coyle insists, are inherently flawed and do not sufficiently represent the reality of economic activity and value. That poses an immense problem for policymakers and analysts, distorting their view of the world and potentially leading them to faulty conclusions and ineffective policies."

The problem is multi-faceted. GDP and other metrics were institutionalized in the industrial age, where agriculture and factory production were easy to measure. As these sectors' share of the economy has slipped, the "hard-to-measure" parts of the economy are now dominant--81.5% by one estimate.

There are many other critical wrinkles in measuring the economy as it is. The book raises the issue of unpaid work, such as families caring for elderly parents and the unpaid "shadow work" that we're required to do now to keep all of our technology functioning. All this activity occurs outside the traditional market.

Since our metrics don't put a price tag on clean air and functional ecosystems, these are left out of the calculations, as if they don't exist. Not only do they exist, they're critical to our well-being. The book discusses natural capital accounting as an alternative, but alternative measures like this are inherently more challenging than toting up transactions.

What if we decided to measure the economy by the quality of life of the citizenry? While there are endless possibilities of what goes into quality of life, we can start with these basics:

1. Our physical and mental health.

2. The health of our social order--our social contract, social trust, communities and trust in our key institutions

3. The security and stability of our livelihoods and financial future.

Defining health isn't that difficult. A healthy person doesn't need any medications because, well, they're healthy, so there's no need for any interventions. A healthy person has an HDL / triglyceride ratio (calculated by dividing your triglyceride level by your HDL cholesterol level) well under 2, can walk a mile without even noticing, can stand on each foot for an extended time, and so on.

As for mental health, numerous studies have found that social connections are critical to our overall health, along with what we might call sufficiency--enough financial resources to secure the basics of life, and enough opportunities to fulfill one's potential.

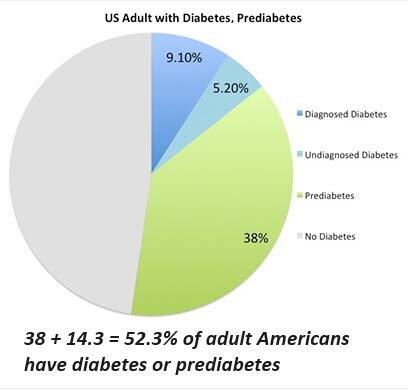

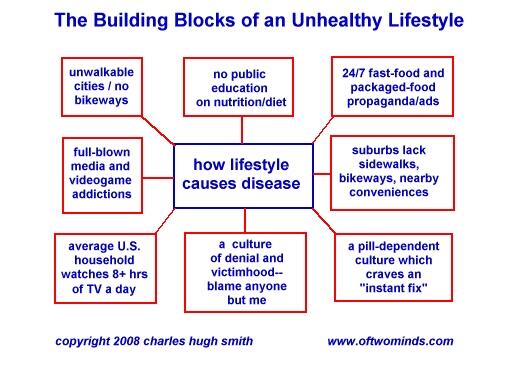

Let's go through some charts of what we already measure. Here is a chart of our metabolic health. Over 50% of adult Americans are diabetic or prediabetic. This is a serious disease that shortens our lives.

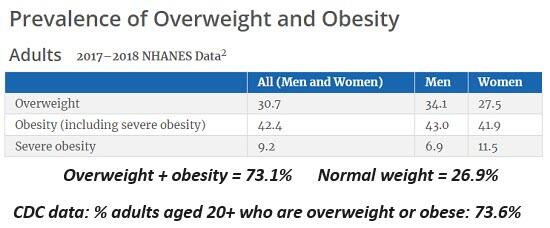

Only a quarter of the adult population is normal (i.e. healthy) weight, reflecting an unhealthy lifestyle of processed foods and inactivity.

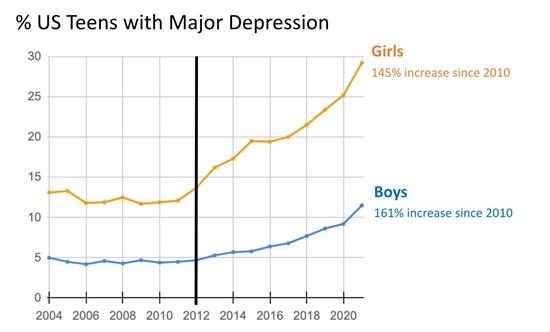

As for mental health, consider teen depression rates. Teen suicide rates have also risen. There is no way to interpret this as healthy.

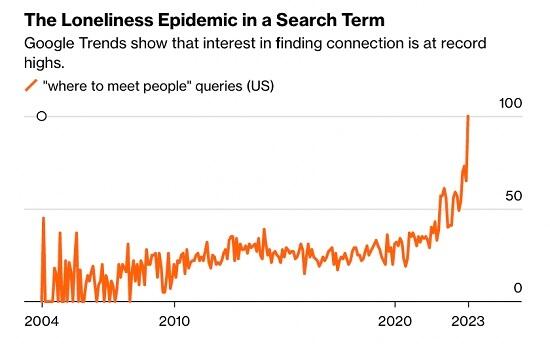

Loneliness--a measure of declining social connections--is also rising sharply.

I prepared this chart of our unhealthy lifestyle and built environment in 2008. Nothing has changed. We can try to sugarcoat all these, but sugarcoating doesn't change reality.

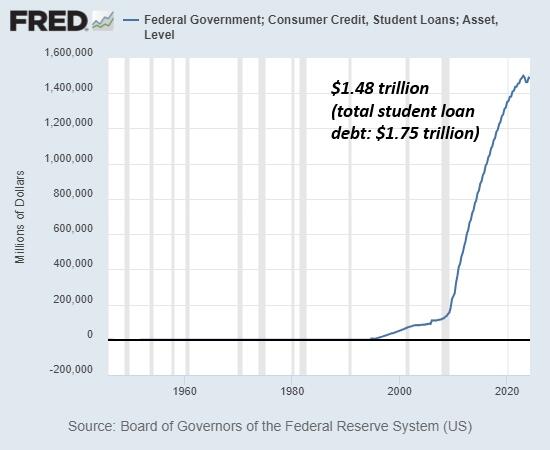

Turning to the social and economic sources of stability, security and opportunity, consider the astounding rise of student loan debt, as attending college / university went from being affordable to requiring lifetime debt serfdom.

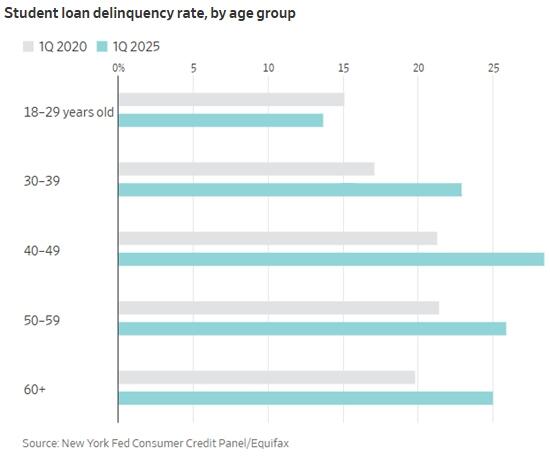

Student loan delinquencies reflect precarity and insecurity, not prosperity and security.

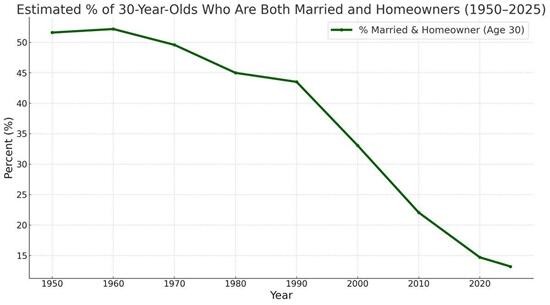

As for opportunity in an economy and society that claims to be a "level playing field," the benchmarks of middle-class security are no longer within reach. The number of 30-year olds who are both married and homeowners has plummeted. Yes, we can quibble about statistics like this, but quibbles are apologists' favorite tools: it's not so bad. But this is just more sugarcoating.

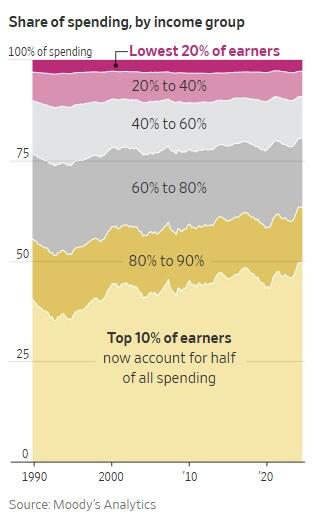

This chart of spending by income group reveals an enormous wealth-income divide. The top 10% collect virtually all the unearned income (from investments), collect over 40% of all the earned income and account for half of consumer spending. The bottom 60%--200 million Americans--account for one-quarter of total spending--half of what the top 10% (34 million Americans) spend.

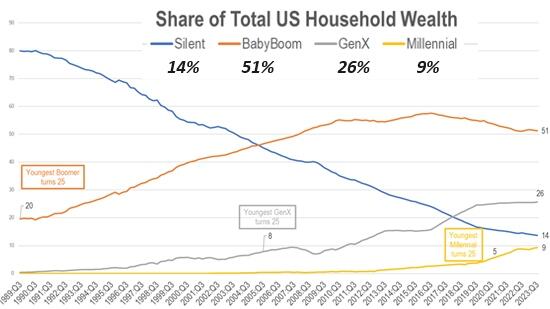

The chart of generational wealth indicates opportunities to build wealth were more accessible pre-2000. Those graduating from high school or university in 2008 or later experienced a much different economy than their parents.

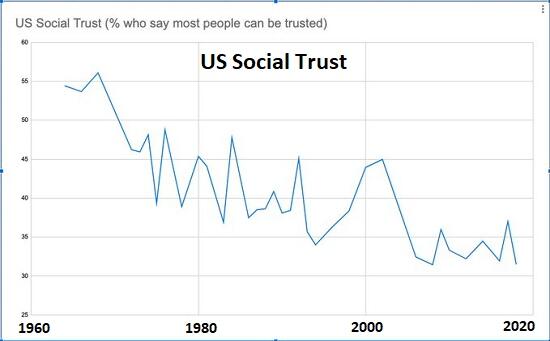

The health of the society is a key element in stability, security and opportunity. Social trust is eroding.

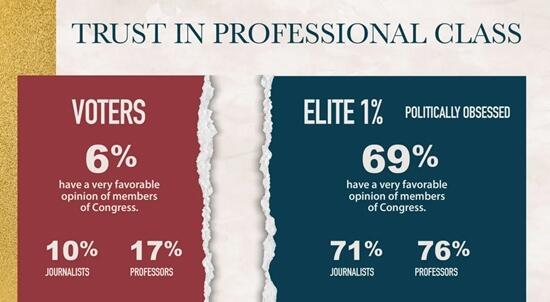

Trust in elites and institutions reflects the wealth-income divide. The top 10% reckon everything's going great because they're doing great. Meanwhile, the bottom 90% live in a completely different world.

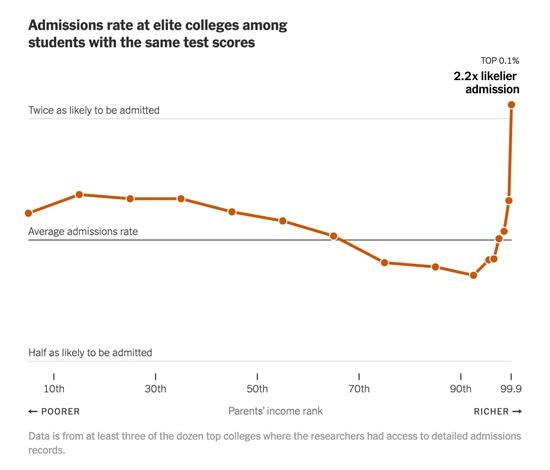

Being born into a wealthy household offers numerous advantages that are difficult for those without these advantages to match. Admissions to elite university reflect this divide. This reflects a neofeudal economy and social order.

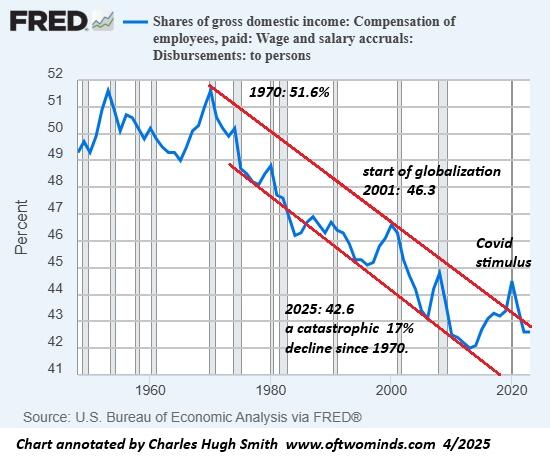

The wealthy own the vast majority of income-generating assets. The majority depend on wages for their living. The decline of wages' share of the economy over the past 50 years is consequential, reflecting the cumulative transfer of $150 trillion from wage earners to capital over the past five decades.

Wealth and income inequality has reached levels that do not reflect a healthy economy or social order.

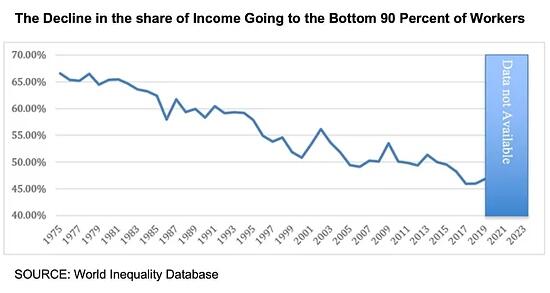

The share of income going to the bottom 90% has declined.

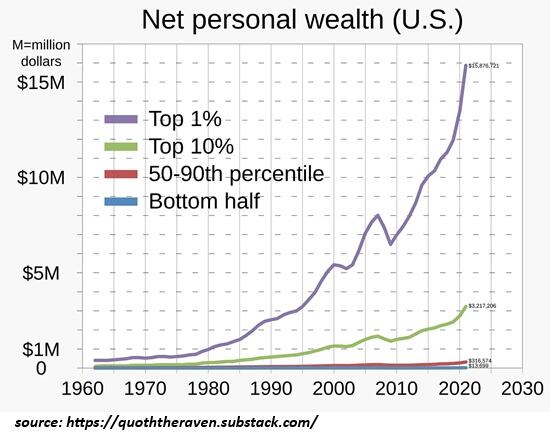

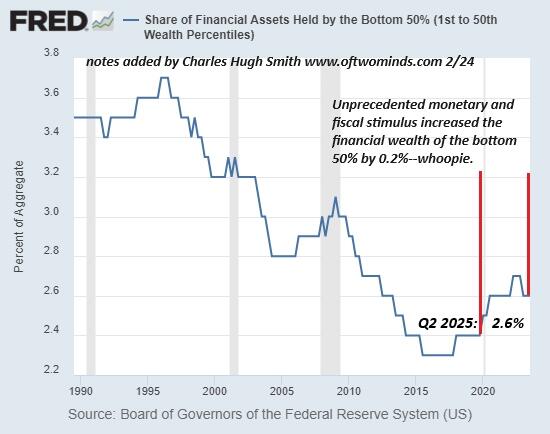

The bottom 50% of American households own a tiny slice of the nation's financial wealth. The vast expansion of central bank stimulus and the resulting asset bubbles haven't increased the wealth of the bottom 170 million Americans, which hovers at 2.6%--signal noise compared to the 31% owned by the top 1% and the 68% owned by the top 10%.

How would we rate the US economy in terms of quality of life? It's clear that we'd have to conclude it's in a deep Depression. Can we really sugarcoat all this with claims everything's going great because GDP is rising and AI is making some of us rich?

As for all the cheerleading about how great the economy is doing--GDP is like collecting data on passenger satisfaction with the dessert cart on the Titanic and declaring everyone is delighted as the great "unsinkable" ship settles into the icy waters of the Atlantic.

"Outraged" Trump Refuses To Adhere To Global Carbon Tax On Shipping

The United States will vote “no” to a global carbon tax proposed by the International Maritime Organization (IMO) on Oct. 17, President Donald Trump said on Truth Social.

“I am outraged that the International Maritime Organization is voting in London this week to pass a global Carbon Tax,” he said in the post on Oct. 16, urging others to reject the proposal.

“The United States will NOT stand for this Global Green New Scam Tax on Shipping, and will not adhere to it in any way, shape, or form.

“We will not tolerate increased prices on American Consumers OR the creation of a Green New Scam Bureaucracy to spend YOUR money on their Green dreams.”

The net-zero framework proposal that was put before the U.N. agency specializing in regulating marine transport would require ships to comply with a global fuel standard for large oceangoing vessels, 5,000 tons or larger, to force the shipping industry’s greenhouse gas emissions down to net zero by 2050.

Signed by Secretary of State Marco Rubio, Secretary of Commerce Howard Lutnick, Secretary of Energy Chris Wright, and Secretary of Transportation Sean Duffy, the statement declared that the United States would retaliate against any of the member states of the IMO that backed it, stating it would be a global carbon tax that “harms the interests of the American people.”

“Under this framework, ships would have to pay fees for failing to meet unattainable fuel standards and emissions targets. These fees will drive up energy and transportation, and leisure cruise costs,” the statement read.

“Our fellow IMO members should be on notice that we will look for their support against this action and not hesitate to retaliate or explore remedies for our citizens should this endeavor fail,” it stated.

“We will fight hard to protect the American people and their economic interests.”

A vote would only occur at the IMO if member states do not agree upon a proposed regulation.

There are 176 member states of the IMO, but a passing vote would require a two-thirds majority of only the 108 member states that ratified previous legislation aiming to reduce shipping pollution.

If passed, the global emissions tax would take effect in 2027 and become “the first in the world” to impose greenhouse gas pricing and mandatory emission limits across an entire industry sector.

The Epoch Times has reached out to the IMO for a response to the U.S. president’s statement.

"The World Is Changing More Rapidly Than Anyone Could Have Imagined A Few Months Ago"

By Elwin de Groot, head of macro strategy at Rabobank

Whatever...

US equity markets extended their losses yesterday as bond yields fell on the back of a decline in US regional bank shares. The S&P index lost 0.6%, the yield on 10y UST’s dropped more than 5 basis points. The market had the finger pointed at the collapse of the subprime auto lender Tricolor Holdings, underscoring the increased sensitivity of the equity market at these elevated levels. Meanwhile, the IMF said it sees “significant downside risks” to global growth following the renewed tensions between the US and China.

Bloomberg writes that Argentinians are dumping the peso, as they believe a devaluation is unavoidable. This potentially undermines the rescue package, including a $20bn swap line, put up by US Treasury Secretary Scott Bessent. Things likely got worse when, earlier this week, President Trump linked Argentinian leader Javier Milei’s success in the upcoming midterm elections to US support: “If he wins we’re staying with him, and if he doesn’t win we’re gone”, Trump said. That sounds more like a ‘whatever’ than a ‘whatever it takes’ US strategy …

French PM Lecornu can already buy himself an “I’m a survivor” t-shirt after surviving two confidence votes yesterday. Whether he survives the looming budget debate is another matter, as his fate now rests with MPs willing to back the budget. If the government sticks to its pledge not to invoke Article 49.3, a majority must actually vote for it.

Socialists leader Olivier Faure warned: “If parliament is not respected and the pension reform isn’t suspended, we would censure immediately.” Markets, meanwhile, are back at square one: the 10-year yield spread narrowed to 76bp from 86bp last week, and the CAC-40 erased October losses—though spreads remain wider than before Bayrou’s confidence vote announcement in August. MNI quoted EU officials saying the “New Fiscal Rules give Lecornu Budget leeway.” Where have we heard that before?

Macron and Lecornu have bought time, but France’s fiscal—and economic—challenges remain.

Beyond Paris, the global stage looks increasingly like an “eat or be eaten” arena where statecraft tools dominate. Wielding such tools successfully, however, is reserved for the ‘happy few,’ requiring economic heft, financial reach, strategic commodities, a strong bureaucracy, political agility, and military muscle.

That explains why small but wealthy economies like Switzerland drew the short straw: since August 7, Swiss goods face a 39% tariff—except generic drugs and Ticino-refined gold. It explains why weaker economies, especially in Africa, struggle against dumping practices due to weak frameworks and enforcement. It explains why several Asian nations agreed to lower tariffs on U.S. goods in exchange for still-high U.S. tariffs. And even the economically large but politically and militarily weaker EU faces limits. Meanwhile, if you have the commodities, you call the shots: Qatar warned yesterday it may halt business with the EU—including LNG supplies—unless Brussels revises its corporate sustainability rules, Reuters reported.

The US has demonstrated the clearest examples of applying such statecraft, as highlighted by our global strategist Michael Every. Presumably, also, because the US does hold the strongest cards (or at least thinks it holds them). This week and last, it was China’s turn to show it has such statecraft cards up its sleeve. It has introduced port fees for US ships (in response to the US port fees on Chinese built/operated ships coming into effect on 14 October) and underscored its dominance in critical raw materials, particularly rare earths, with a further tightening of its export controls regime.

Whether both players have a full grasp of their own and their opponent’s tools and power(s) remains an open question; uncertainty over that may actually be the strongest guardrail to prevent this power struggle from running completely out of control. That said, it’s even harder to see the spirit going back into the bottle. In other words, the world is changing more rapidly and profoundly than many would have imagined only a few months ago.

And the US keeps trying to drag its allies into its statecraft framework - “President Trump has instructed the ambassador and myself to tell our European allies that we would be in favour of whether you would call it a ‘Russian oil tariff’ on China or a ‘Ukrainian victory tariff’ on China,” Mr Bessent told reporters in Washington on Wednesday. “But our Ukrainian or European allies have to be willing to follow. We will respond if our European partners will join us.”

The strategy would introduce a 500 per cent levy on imports from China, with the money generated being used on weapons for Ukraine’s military. 500 is obviously Trump-style language, -and would effectively be counterproductive as it would halt most trade with tariff revenue close to nothing- but it does carry a serious undertone and the line of reasoning more fits ‘decoupling’ than ‘de-risking’.

For Europe de-coupling seems like no entry territory (unless China would truly block critical raw materials to European markets ?). It explains why Europe is often portrayed as the one being ‘squeezed’ in the middle. Whilst that remains a useful framing of the overall global picture, Europe is not standing still completely. The lack of key enabling factors such as military strength and political agility (read: unity) are visibly slowing things down, however.

For example, the EU has been slow with the implementation of its Competitiveness Compass agenda (a descendant from the 20204 Draghi and Letta reports); The ‘Draghi Observatory’ concluded in September that out of 383 recommendations, only 11.2% have been fully delivered.

That said, the European Commission (EC) is intensifying trade defense measures, making 2025 a record year for anti-dumping tariffs and protectionist actions. On 7 October, it proposed a new steel safeguard regime to replace the current system in July 2026, cutting tariff-free import volumes by 47% and doubling out-of-quota tariffs to 50%, a move partly influenced by the recent US-EU framework agreement. The EC is also considering pre-conditions for Chinese investments in Europe, such as mandatory technology transfers, signaling a strategic shift toward statecraft. Meanwhile, the EU announced it has achieved its €300 billion Global Gateway investment target two years early, focusing on sustainable infrastructure and strategic corridors, particularly in Africa, to rival China’s Belt and Road.

Energy independence remains a priority, with plans to ban Russian oil imports by early 2026 and gas by 2027, pending (final) parliamentary approval. At the Copenhagen summit (1–2 October), leaders debated strengthening EU defense capabilities, including a proposed “European Drone Wall,” though feasibility concerns persist. Discussions also revealed divisions over a €140 billion interest-free loan for Ukraine funded by frozen Russian assets, despite Germany softening its stance. A plan to “buy European” in public procurement - to boost domestic firms and counterbalance protectionist US trade policies as well as China’s weaponization of critical dependencies - is also in the works. But countries haggle about the definition of ‘European’. Overall, the EC’s actions underscore a more assertive and strategic EU posture globally, but it obviously cannot match the depth and speed of the US.

The EU yesterday unveiled a five-year defense roadmap aimed at closing critical capability gaps and modernizing its security architecture.

The plan introduces four flagship initiatives: